Busting myths about disability cover

We routinely insure our homes, cars, health and ourselves, but insuring against disability often gets overlooked, especially when we're healthy and focused on building our future. However, it's a crucial part of a robust financial plan, but navigating the options can be confusing, especially with common misconceptions floating around.

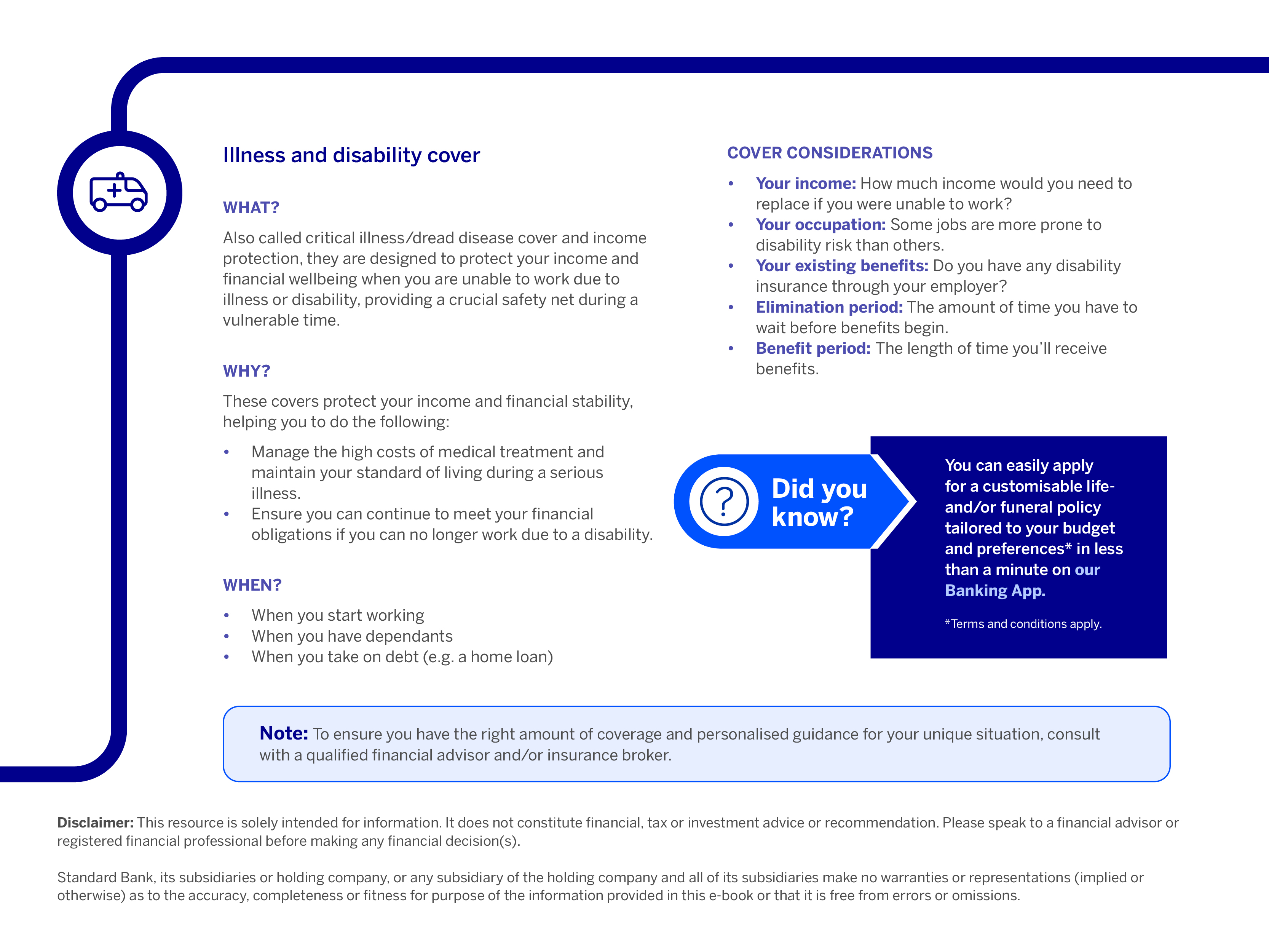

Disability cover is a type of insurance designed to provide financial support if you become unable to work and earn an income due to becoming permanently disabled. It acts as a safety net to help you maintain your financial stability when your income stops.

Let's cut through the noise and separate fact from fiction to help you make informed decisions about protecting your financial future.

Why get disability cover?

Your ability to earn an income is a valuable asset and losing that ability can have a devastating impact on your finances and lifestyle and your family’s wellbeing. Disability cover can help you protect your financial stability by paying out a lump sum which can be used for expenses, such as paying off debt, modifying your home to accommodate your disability, funding long-term care or reinvesting it for future income.

Having the right protection in place means you won’t have to deplete your savings or go into debt to pay your bills, and your family could continue living without drastic financial adjustments during a challenging time. It can also help pay for additional medical costs, specialist care or assistive equipment not covered by medical aid.

Myth #1: It won’t happen to me

Fact: It’s natural to believe that serious illness or injury only happens to others, but life is inherently unpredictable. Disability can affect anyone, regardless of age, health or profession. A sudden accident, a chronic illness or an unexpected health condition can strike at any time, making it impossible to continue working and therefore continue earning money.

Thinking ‘it won't happen to me’ leaves you vulnerable. Instead, consider disability cover as a crucial part of planning for the unexpected, much like insuring your car or home. It's about protecting your earning potential, the engine that drives your financial life.

Myth #2: My workplace benefits are enough

Fact: While some employers offer group disability benefits, relying solely on them can leave you exposed. These benefits often cover only a limited percentage of your salary, might have a very strict definition of what counts as disabled and typically end if you leave the company. Plus, payments might only last for a set period, even if you're still unable to work long term.

Take the time to understand your company's policy: how much it pays, what disability means to them and what happens if you change jobs. This will help you see where personal disability cover might be needed to fill any gaps and truly protect your income.

Myth #3: I’ll always be covered by workmen’s compensation

Fact: Workmen's compensation is specifically for injuries or illnesses that happen at work or because of your job. While important for workplace incidents, it has big limitations because it doesn’t cover you becoming disabled outside of work.

Therefore, if you get into an accident outside of work (e.g. car crash on holiday) or suffer a long-term health issue, you simply aren’t covered. Even for work-related problems, the benefits might not fully replace your income or cover all your long-term needs.

Relying only on this leaves you vulnerable to many common life events that could stop you from working and earning an income. Disability cover steps in to bridge this crucial gap, protecting you financially from the wide range of ways disability can arise.

Ensure your financial stability against life's unpredictable challenges

Don't let misconceptions leave your financial future vulnerable. Review your current financial situation, assess your potential needs and consider speaking with a qualified financial advisor and/or insurance broker to help you explore options and tailor a solution to suit your circumstances.

*Terms and conditions apply

Disclaimer: This article is solely intended for information. It does not constitute financial, tax or investment advice or recommendation. Please speak to a financial advisor or registered financial professional before making any financial decision(s).

Standard Bank, its subsidiaries or holding company, or any subsidiary of the holding company and all of its subsidiaries make no warranties or representations (implied or otherwise) as to the accuracy, completeness or fitness for purpose of the information provided in this article or that it is free from errors or omissions.

Want to know more about insurance?

Download our free Insurance essentials e-book and learn more about the different types of insurance.

Related articles and media