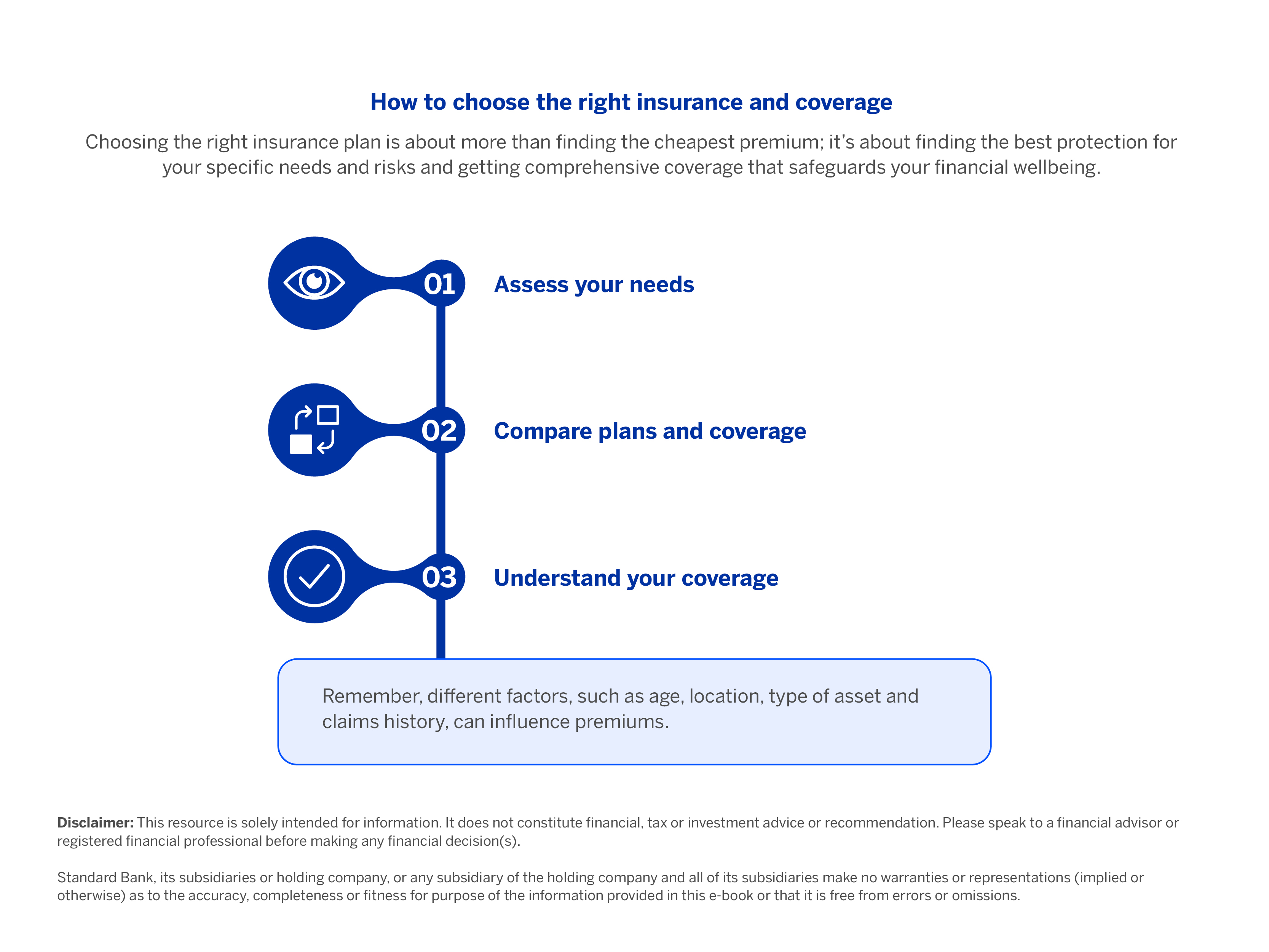

Life cover: Everything you need to know

Planning and providing for the wellbeing of your family includes safeguarding their financial future even if the worst occurred. Among the various options available, life cover, also known as life insurance, serves as a financial tool designed to offer support and stability during challenging times when people pass away.

Planning and providing for the wellbeing of your family includes safeguarding their financial future even if the worst occurred. Among the various options available, life cover, also known as life insurance, serves as a financial tool designed to offer support and stability during challenging times when people pass away.

Imagine the comfort of knowing that, even in the toughest times, your family can still cover daily living costs, manage debts or ensure their education expenses are met. It’s about securing their stability when they need it most and providing a way to ensure that financial responsibilities can be managed should the unexpected occur.

What is the difference between life and funeral insurance?

Life insurance and funeral insurance each serve important but distinct purposes. Life insurance provides a lump-sum payout to your beneficiaries in the event of your death with the purpose of these funds being to help cover living expenses, debts or future goals such as education costs over the medium to long term.

Funeral insurance, also known as funeral cover, is designed to assist with covering funeral, burial and other end-of-life expenses. It’s designed to ease the immediate financial burden on your loved ones during a difficult time, allowing them to grieve without added financial stress.

When should I get life insurance?

The notion that life cover is only needed later in life is a misconception. If you have dependants, financial responsibilities or outstanding debts, life cover can help secure your family’s financial future. Even if you’re single, other forms of cover such as disability or critical illness protection can prevent financial hardship if you’re unable to earn an income.

Different types of coverage exist, and it can be customised to your needs. It’s also important to know that every policy has specific terms, conditions and exclusions, and knowing your options upfront can help you choose cover that fits your unique life circumstances.

How does life cover work?

When you choose to take out life cover, you agree to make regular payments, known as premiums (typically monthly), and in return for these payments, your insurer promises to provide a financial payout in the event of a death.

Should the person covered by the policy pass away, the insurer will pay out a predetermined lump sum of money. This payment is directed to your nominated beneficiaries, the individual(s) or entities you've chosen to receive the funds, or to your estate if no specific beneficiaries are named.

How much life cover do I need?

The amount of this lump sum depends on the level of cover you selected when you established your policy, and it's always guided by its specific terms and conditions. The amount of cover you qualify for will depend on a few key factors, including your age, health, income, lifestyle habits and occupation. Insurers use these factors to assess your overall risk profile and determine the level of cover that’s most suitable for you.

Since every person’s financial situation is unique, it’s a good idea to speak to a qualified financial adviser and/or insurance broker who can help assess your needs and assist with choosing the right amount of coverage. This ensures you’re neither over- nor underinsured and that you understand how your cover fits into your broader financial plan.

|

Important: You can’t take out new cover once you become seriously ill or disabled and any pre-existing conditions can affect your coverage. Therefore, starting life insurance early typically not only ensures eligibility before potential health changes but will also likely secure more affordable premiums as your risk profile will be lower when you’re younger and healthier. |

Ready to get customised life cover?

Explore the benefits of our Flexible Life Plan and get your free quote today.

*Terms and conditions apply

Disclaimer: This article is solely intended for information. It does not constitute financial, tax or investment advice or recommendation. Please speak to a financial advisor or registered financial professional before making any financial decision(s).

Standard Bank, its subsidiaries or holding company, or any subsidiary of the holding company and all of its subsidiaries make no warranties or representations (implied or otherwise) as to the accuracy, completeness or fitness for purpose of the information provided in this article or that it is free from errors or omissions.

Related articles and media